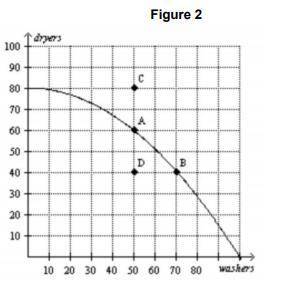

This economy cannot currently produce 70 washers and 70 dryers because a. it is not using all of its resources. b. it is not using the most efficient production process. c. it does not have the resources and technology to produce that level of output. d. all of the above are correct

Answers: 1

Another question on Business

Business, 21.06.2019 22:30

Emily sold the following investments during the year: stock date purchased date sold sales price cost basis a. 1,000 shares dot com co. 03-21-2007 02-04-2018 $20,000 $5,000 b. 500 shares big box store 05-19-2017 01-22-2018 $8,200 $7,500 c. 300 shares lotta fun, inc. 10-02-2017 09-21-2018 $3,000 $4,500 d. 700 shares local gas co. 06-17-2017 11-11-2018 $14,000 $17,000 for each stock, calculate the amount and the nature of the gain or loss.

Answers: 3

Business, 22.06.2019 02:00

4. suppose that pollution in a neighborhood comes from two factories, with marginal benefit curves given by mb1 = 12 – p1 and mb2 = 8 – p2. the level of pollution in the neighborhood is given by p = p1 + p2. the government wants to limit pollution by instituting a pollution-rights market. the government’s desired level of p is 10, so it prints 10 pollution rights and offers them for sale to the firms.a)find the equilibrium selling price of a pollution right, as well as the allocation of rights (and hence pollution levels) across the two factories. b)repeat part (a) for the case where the government’s desired level of pollution equals 14. c)comment on the usefulness of a pollution rights market in achieving efficient levels of pollution abatement.

Answers: 2

Business, 23.06.2019 07:00

Nthis economy, community members typically use simple tools to plant and harvest crops. food supplies are supplemented by hunting animals and gathering plant materials. members trade with each other to obtain needed goods, as few people hold currency. little economic growth occurs. what type of economy is being described?

Answers: 3

Business, 23.06.2019 07:40

In the short-run, marginal costs are equal to the change in variable costs as output changes. ( mc = change in variable cost / change in quantity) assume that capital is fixed in the short-run. (a) start with the equation for marginal cost and derive an equation that relates marginal cost of production to the cost and productivity of labor. (b) draw a standard looking short-run marginal cost curve and use the equation you derived to explain its shape.

Answers: 2

You know the right answer?

This economy cannot currently produce 70 washers and 70 dryers because a. it is not using all of its...

Questions

Mathematics, 05.05.2021 01:00

Chemistry, 05.05.2021 01:00

Mathematics, 05.05.2021 01:00

Mathematics, 05.05.2021 01:00

Computers and Technology, 05.05.2021 01:00

Mathematics, 05.05.2021 01:00

Computers and Technology, 05.05.2021 01:00

Mathematics, 05.05.2021 01:00

Mathematics, 05.05.2021 01:00

Biology, 05.05.2021 01:00

Social Studies, 05.05.2021 01:00