Defination of Asset :

An Asset forms a very key part of a business organization which could be defined as

‘the economic resources held by an entity due to its past activities through which entity will have future economic benefits as well as future cash flow in the long term run of the business in the future

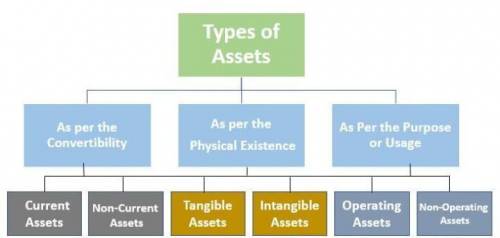

i.e., current assets, non-current assets, tangible assets, intangible assets, operating assets, non-operating assets.

Types of Asset :

1 . As per the Convertibility

This bifurcation is done as per the terms or periods required for the convertibility of assets into liquid assets or Cash & Cash equivalents which could be either of the two:

• Current Assets :

Current Assets are the assets that are easily convertible into liquid assets or cash & cash equivalents.

In terms of period, the current assets are the assets, which on requirement could be converted into liquid assets within a period of a year or 12 months.

Examples of such assets are short-term deposits, inventories, marketable securities, prepaid expenses, Trade or Accounts Receivables, etc.

•Non-Current Assets:

Non-Current Assets are also known as Long term Assets which are not easily convertible into liquid assets as compare to the current assets.

In terms of the period of conversion, the non-current assets usually take more than a year for conversion into liquid assets and are productive for business for more than a year.

Examples of such assets are fixed assets like land, Plant & Machinery, Buildings, vehicles & Trademarks etc.

2. As per the Physical Existence

This Bifurcation is done as per the physical existence of the assets as if the assets physically exist or the asset body physically exist or not and as per nature, the assets could be bifurcated into two parts:

•Tangible Assets :

Tangible assets are the assets that physical exist and they can be seen, felt, and touched by us and through which the business entity generate future economic profits and generate cash flows.

Examples of such assets are Fixed Assets like plant & Machinery, lands, buildings, vehicles, furniture, etc. All of the fixed assets fall under the category of tangible assets.

• Intangible Assets

Intangible assets are basically the assets whose physical form does not exist and could not be touched or felt by us but are essential assets to the business entity as the entity generates cash flow through them and as well as expected to derive future cash flows as well as economic benefits from them.

Examples : Goodwill, Patents, Copyrightes etc.

3. As Per the Purpose or Usage

This Bifurcation is done as per the actual usage of the asset i.e., the assets which are used on daily basis and are economically responsible for cash inflows or the assets which are kept or collected & are not used on daily basis but would be converted or benefited for some specific purpose at future date. Such types of assets could be categorized in two:

• Operating Assets :

Operating Assets are the assets, which are kept and used on a daily basis in the business for daily business operations. Such assets are part of every necessary operation of the business and some of the examples are plant & machinery, inventories, Buildings, equipment, trademarks, cash & cash equivalents, etc.

These assets are used to derive cash flow & business operations through the basic & common business activities of the entity.

• Non-Operating Assets :

Non-operating assets are a little different from the operating assets. As operating assets are used in daily business operations and the revenue is generated on daily basis but non-operating assets are the assets, which are store, accumulated, or hold onto by the entity to generate cash flow in the future.

2. Batteries store chemical energy and convert it to electrical energy, which can be thought of as the flow of electrons from one place to another. In a battery, components called electrodes help to create this flow