Mathematics, 21.12.2019 07:31 zhenhe3423

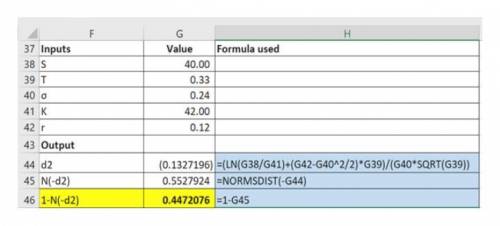

The price of a certain security follows a geometric brownian motion with drift parameter µ = 0.12 and the volatility parameter σ = 0.24.

(a) if the current price of the security is $40, find the probability that a call option, having four months until expiration and with a strike price of k = 42 will be exercised.

(b) in addition to the above information as in part (a) if the interest rate is 8%, find the risk-neutral arbitrage free valuation of the call option.

Answers: 2

Another question on Mathematics

Mathematics, 21.06.2019 22:20

Which strategy is used by public health to reduce the incidence of food poisoning?

Answers: 1

Mathematics, 21.06.2019 22:30

Fast! find the length of cu. the triangles are similar. show your work.

Answers: 2

Mathematics, 21.06.2019 23:00

Acaterer knows he will need 60, 50, 80, 40 and 50 dinner napkins on five successive evenings. he can purchase new napkins initially at 25 cents each, after which he can have dirty napkins laundered by a fast one-day laundry service (i.e., dirty napkins given at the end of the day will be ready for use the following day) at 15 cents each, or by a slow two-day service at 8 cents each or both. the caterer wants to know how many napkins he should purchase initially and how many dirty napkins should be laundered by fast and slow service on each of the days in order to minimize his total costs. formulate the caterer’s problem as a linear program as follows (you must state any assumptions you make): a. define all variables clearly. how many are there? b. write out the constraints that must be satisfied, briefly explaining each. (do not simplify.) write out the objective function to be minimized. (do not simplify.)

Answers: 1

Mathematics, 21.06.2019 23:30

If you measured the width of a window in inches and then in feet with measurement would you have the greater number of units

Answers: 3

You know the right answer?

The price of a certain security follows a geometric brownian motion with drift parameter µ = 0.12 an...

Questions

Mathematics, 13.11.2020 02:40

Computers and Technology, 13.11.2020 02:40

Computers and Technology, 13.11.2020 02:40

Mathematics, 13.11.2020 02:40

Social Studies, 13.11.2020 02:40

Mathematics, 13.11.2020 02:40

Mathematics, 13.11.2020 02:40

Mathematics, 13.11.2020 02:40

Mathematics, 13.11.2020 02:40

English, 13.11.2020 02:40

Computers and Technology, 13.11.2020 02:40

Mathematics, 13.11.2020 02:40

Business, 13.11.2020 02:40